This document outlines the taxes currently applicable to Small and Medium Enterprises (SMEs) in Zimbabwe, including details about the presumptive tax and other tax obligations.

1. Presumptive Tax

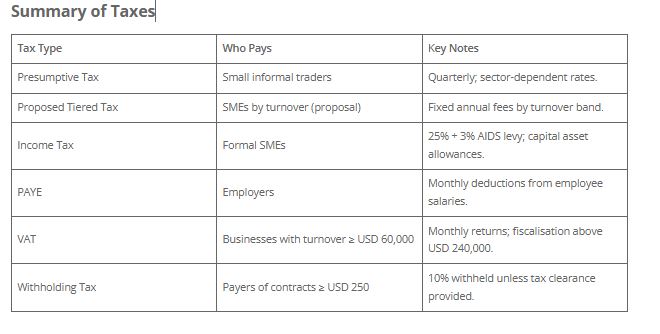

Presumptive tax is a simplified quarterly tax based on estimated earnings for small-scale traders who do not file normal income tax returns. It applies to informal operators such as tuckshops, salons, cross-border traders, small-scale miners, restaurants, and certain transport operators.

Key points:

- • Paid quarterly (due 10 January, April, July, October).

- • Rates vary by business sector.

• Intended to widen the tax base among informal businesses.

2. Who should pay Presumptive taxes?

Businesses not registered for Value-Added Taxes (VAT) and in categories that include the following.

Taxi Operators

Commuter Omnibus Operators

Driving Schools

Cross-border Traders

Hairdressers and Beauticians

Cottage Industries

Small-scale Miners

Informal Traders (e.g., market vendors)

Operators of bottle stores, bars, and restaurants

Property Owners Leasing Out Real Estate

4. Proposed Tiered Presumptive Tax System

A proposal from the Confederation of Zimbabwe Retailers (CZR) suggests a tiered system based on turnover. Although not yet law, the proposed tiers are as follows:

- Turnover up to USD 15,000: USD 500 per year.

- Turnover USD 15,000–50,000: USD 1,500 per year.

- Turnover USD 50,000–100,000: USD 3,000 per year.

5. Income Tax

SMEs that do not qualify for presumptive tax must register and file income tax returns. The corporate tax rate is 25%, plus a 3% AIDS levy. Qualifying capital assets may benefit from a 100% special initial allowance (split across three years).

6. PAYE (Employees’ Tax)

If an SME employs staff, it must register for PAYE within 14 days and withhold tax from employee salaries monthly, based on ZIMRA tax tables.

7. Value-Added Tax (VAT)

Businesses with an annual turnover above USD 60,000 must register for VAT. They must submit returns and remit VAT by the 25th of the following month. Fiscalisation is mandatory for businesses with turnover above USD 240,000.

8. Withholding Tax

A 10% withholding tax applies to contract payments exceeding USD 250, unless the recipient provides a valid tax clearance certificate.