By Hillary Munedzi

As Zimbabwe struggles to rebuild its economy, the tax system has become both a lifeline and a liability. For government, taxes remain the primary revenue stream. For businesses, they are a maze of levies, duties, and shifting rules that erode competitiveness. The question is no longer “what can we tax?” but “do businesses trust the tax system?” Without trust, compliance collapses—and so does growth.

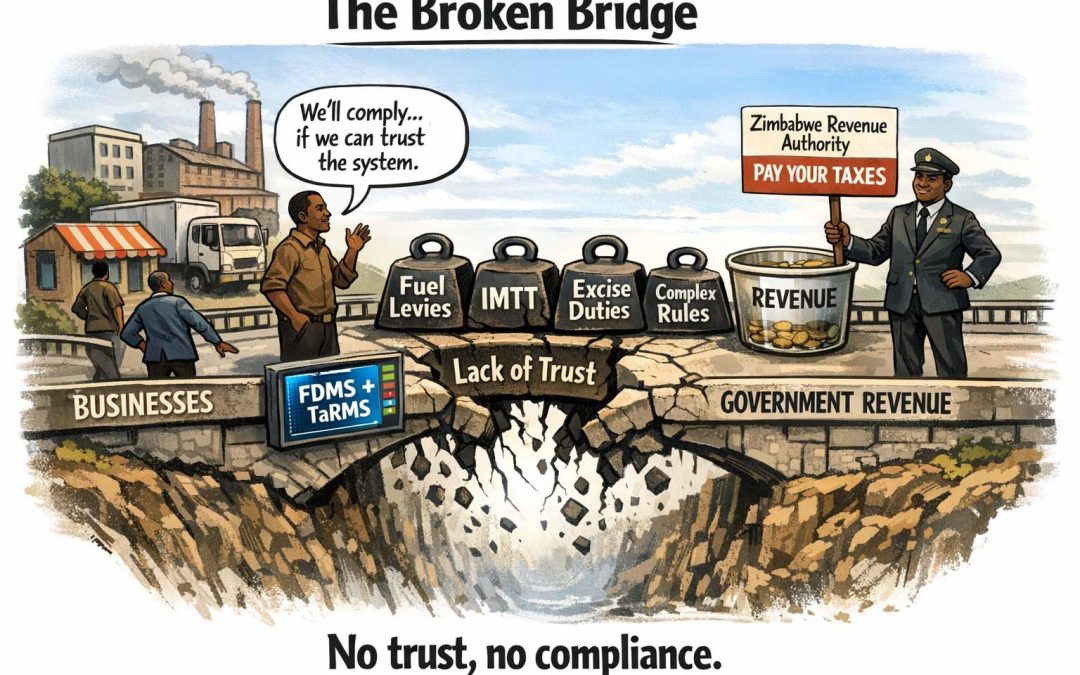

Complexity and Instability

Zimbabwe’s tax regime is notorious for its unpredictability. Frequent currency changes, shifting regulations, and overlapping levies make long-term planning nearly impossible. Foreign investors, already wary of macroeconomic instability, see this as a red flag. For local firms, the burden is heavier still: inflation eats margins while compliance costs mount. The constant recalibration of tax heads undermines confidence, leaving businesses unsure of what tomorrow’s obligations will look like.

Fuel Taxes: A Case Study in Burden

The government’s decision in May 2025 to raise the fuel levy to US$0.2470 per litre for petrol and US$0.1870 for diesel illustrates the dilemma. Intended to shore up reserves, the hikes pushed Zimbabwe’s fuel prices above US$2 per litre, second only to Malawi in the region. For transport operators, manufacturers, and miners, this levy is not just a tax—it is a competitiveness killer. Rising logistics costs ripple across the economy, inflating consumer prices and squeezing margins in already fragile industries.

Formal Businesses Carry the Load

Large corporations, already more compliant than SMEs, bear the brunt of these taxes. Excise duties, the Intermediated Money Transfer Tax (IMTT), sugar taxes, and now fuel levies pile onto operational costs. Meanwhile, smaller enterprises often slip through the cracks, widening the compliance gap and discouraging formalization. The result is a distorted system where those who play by the rules are penalized, while those outside the net escape scrutiny.

Digital Modernization: FDMS-TaRMS Integration

The Zimbabwe Revenue Authority (ZIMRA) has taken steps toward modernization by integrating the Fiscalisation Data Management System (FDMS) with the Tax and Revenue Management System (TaRMS). Real-time transaction capture, automated VAT returns, and audit trails promise transparency. By eliminating manual data entry and enabling pre-filled schedules, the system could reduce compliance costs and errors. Yet technology alone cannot rebuild trust. If businesses suspect data manipulation or fear misuse of personal information, adoption will stall.

Trust as the Cornerstone

True reform requires cultural transformation. ZIMRA must shift from an enforcement-heavy posture to a service-oriented one. Predictability, fairness, and transparency—not just digital dashboards—will convince businesses that compliance is in their interest. A tax system that is seen as punitive will always invite avoidance. A system that is seen as fair, efficient, and predictable will foster voluntary compliance.

The Pan-African Context

Zimbabwe’s struggle is not unique. Across Africa, governments face the same tension: raising revenue without strangling growth. Kenya’s iTax and Rwanda’s e-filing show that digital systems can succeed when paired with credibility. These countries built trust by simplifying processes and ensuring transparency. For Zimbabwe, the lesson is clear—trust is the tax base. Without it, even the most sophisticated systems will fail to deliver.

The Road Ahead

Rebuilding tax compliance in Zimbabwe requires more than levies and enforcement. It demands a compact between state and business, built on transparency, predictability, and fairness. The integration of FDMS and TaRMS is a step forward, but it must be accompanied by a broader cultural shift. Only then can Zimbabwe move from a system of coercion to one of confidence—and unlock the growth that compliance makes possible.