by Kuda Musasiwa (aka @begottensun)

⸻

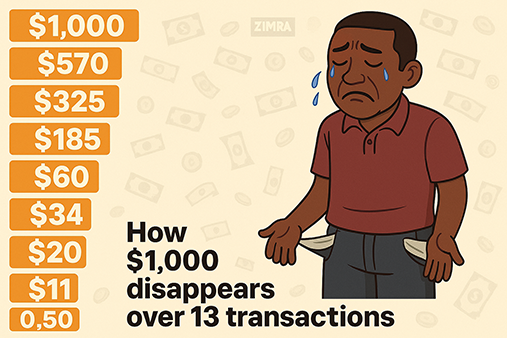

Let us break down what happens when $1,000 enters the Zimbabwean mobile money or bank system.

We are looking at three taxes, namely the 2% intermediated money transfer tax (IMTT), an applicable Ecocash or bank fee of 3 %, and a value-added tax of 15% on applicable goods.

The first step is upon receiving money – when $1,000 hits your wallet, the 2% IMTT is immediately deducted.

This means $20 is deducted and sent to the Zimbabwe Revenue Authority (ZIMRA) leaving a usable balance of $ 980.

This tax is invisible to most, but it already trims your total.

The next step is when you are using the money.

Let us suppose you use the full $980 in 75 equal transactions with each transaction attracting the 2% IMTT tax and the 3% bank or Ecocash fee, making the total fees per payment 5%.

This means only 95% of each payment reaches your supplier.

So, the actual value reaching others is about $ 933.33.

The third step is the tax you pay on spending.

From the $ 933.33, the 2% IMTT on outflows amounts to $ 18.67 and the 3% on bank charges amounts to $28.00.

This equals another $46.67 just for sending money during spending.

The next step is to consider the VAT hidden in the price.

Now, let us suppose 50 of the 75 payments are for goods/services that include 15% VAT.

This means that $622.22 of your spending is VATable.

Since prices already include VAT, we back-calculate it to find what percentage of the $622.22 went to VAT, which gives us $81.16

This VAT never reaches your supplier—it is collected for transmission to ZIMRA.

Thus, the final summary of where your $1000 went shows that the portion collected by ZIMRA is $119.83, the amount going to Ecocash or bank charges is $28 and the actual amount one uses before VAT is $852.18.

The conclusion is that out of your $1,000, only $852.17 reaches the economy (your pocket) as actual value.

And $147.83 is absorbed by the system in taxes and transfer fees.

Every swipe, transfer, and payment is taxed multiple times. Transaction costs add up fast.

This is why cash deals are still king for many—and why financial inclusion must come with cost reform.

NOTE: This article has been edited for readability.